Chapter 1 - When Warming Becomes Uninsurable

Draft Chapter for Sunlight Reflection - The Business Case for an Albedo Accord

Chapter 1 - When Warming Becomes Uninsurable

Insurance provides core financial infrastructure for the economy. If insurers cannot reliably turn a profit, markets close and premiums spike. Whole regions become uninsurable. That is already happening. Over the last decade, global insured losses from natural catastrophes have settled into a new normal above US $100 billion per year, with 2025 again breaking that threshold.[1] Leading reinsurance firms Swiss Re and Munich Re now warn that annual insured losses could plausibly reach US $300 billion in a peak year if a few major hurricanes and earthquakes line up. Insured losses have been growing faster than global GDP for decades.[2]

Munich Re describes the emerging climate threat as follows:

“Natural disasters worldwide: Losses are on the rise as climate change strikes… the visible trend towards increasing losses is driven by … severe thunderstorms, hail, flooding or wildfires – also known as “non-peak perils” or “secondary perils”… studies are providing ever clearer evidence that man-made climate change is playing an increasingly important role in the rising losses… two things are therefore necessary to limit the damage: loss-reducing adaptations to the risk, such as more stable buildings and avoiding construction in high-risk areas, and halting climate change as far as possible… Climate change showed its claws in 2024. Well over 90% of the total losses of US$ 320bn were caused by weather-related catastrophes. According to the latest research, many of the events witnessed are becoming more intense or more frequent. Prevention pays off in the form of lower losses and must therefore be given the highest priority.” [3] [bold added]

The insurance industry depends on global reinsurance companies to absorb the shock of major disasters and to map emerging risks, such as climate change. The reinsurers insure the insurers, taking on a share of the biggest losses so no single company or country has to carry all the risk alone. Reinsurers invest heavily in climate and catastrophe modelling. Their analysts track long-term trends in storms, floods, fires and heatwaves, constantly updating the assumptions that underlie insurance finance. When reinsurers decide that a peril is worsening, it quickly shows up as higher costs, tighter terms or withdrawal of cover. Their models are an early-warning system for the whole economy, signalling when the physical climate is drifting outside the bounds of what can be reliably insured.

For business leaders across the economy, withdrawal of cover is more than an insurance problem.[4] It is a warning that the physical climate is drifting outside the zone where corporate operation is feasible.

This chapter explores that warning. We will explore how global warming is rapidly changing how insurers now talk about secondary perils and “planetary solvency”, what recent disasters tell us about risk, and why “hundred-year” events now feel like regular features of the landscape.

The aim is to show that if warming continues on its current trajectory, growing parts of the real economy will become uninsurable and, in effect, unbankable. A place or asset is unbankable when it is seen as too risky to serve as reliable collateral. Insurers withdraw or sharply reduce cover, banks can no longer trust future asset values, and new mortgages, long-term loans and investment capital largely dry up. Impact on insurance and banking are initial signs of a wider impact of warming on business.

But there is something we can do to prevent this scenario. Cooling the planet can now be recognised as a core business continuity issue, achieving Munich Re’s stated goal that “prevention pays off in the form of lower losses and must therefore be given the highest priority.”

Insurance as the climate’s early warning system

Insurance and reinsurance are, in effect, the climate’s financial seismograph. Just as geologists see small tremors that come before a bigger eruption, insurance collates data from thousands of events, prices the risks, and decides where capital will and will not stand behind physical assets. The insurance tremors are growing.

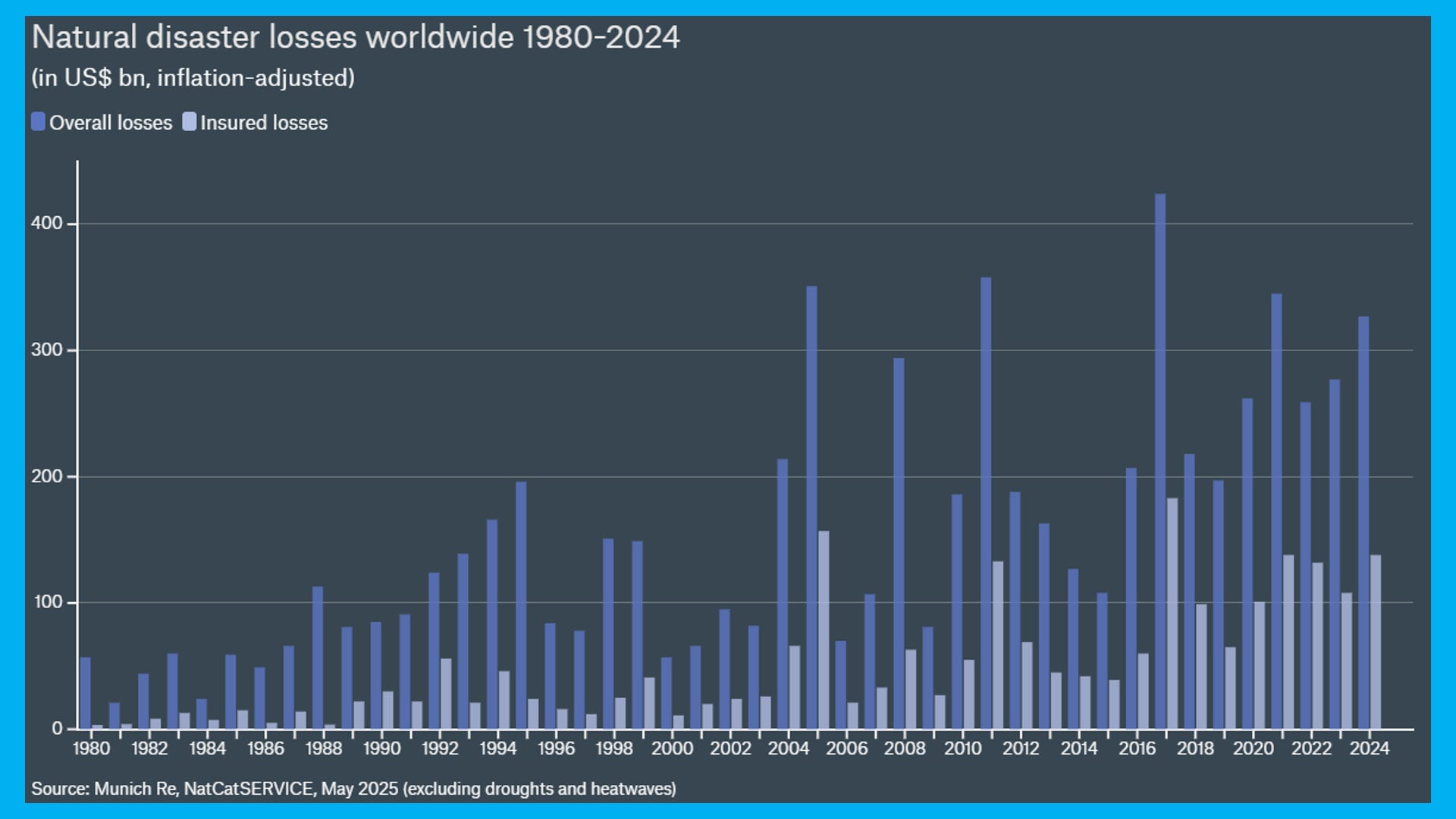

In 2023, natural catastrophes produced about US $108 billion in insured losses worldwide.[5] In 2024, insured losses rose again to around US $140 billion, with total economic losses near US $320 billion.[6] 2025, kicking off with the catastrophic California fires, makes six years in a row above US $100 billion. Over the last 30 years, insured catastrophe losses have grown at around 5–6% per year in real terms, outpacing global GDP growth.[7]

Swiss Re now treats US $100 billion+ in annual insured catastrophic losses as “standard”.[8] This chart from Munich Re shows how much losses have grown.[9]

Even while the industry remains profitable, insurers are withdrawing from high-risk regions and sharply raising premiums. In California and other US states, climate-driven wildfires, floods and landslides are threatening the stability of the insurance market, forcing regulators and governments into difficult choices about who carries the risk.[10]

The lesson for boardrooms is that once the climate pushes a region beyond insurable bounds, other parts of the financial architecture are next in line. Mortgages become harder or more expensive to obtain, asset values fall as buyers price in rising physical risk, and public balance sheets are strained by repeated disaster relief. Insurance is not just another line item. It is a core signal of whether the future climate is compatible with business as usual.

From “peak perils” to “secondary perils”

For much of the modern insurance era, the big worries were known as peak perils: major hurricanes making landfall, large earthquakes, maybe a handful of catastrophic river floods.

That picture has changed. Reinsurers now talk constantly about secondary perils. These include convective storms with resulting large hail, flash floods, rain bombs, atmospheric rivers, wildfires, smoke, flooding and tidal surge from hurricanes and cyclones.[11]

Convective storms are intense thunderstorms driven by convection - rising warm moist air. They are a growing headache for insurers because they can unleash localised but extremely costly damage: giant hail, tornadoes, downbursts and flash floods that shred roofs, smash solar panels and cars, and overwhelm drains in minutes. “Rain bombs” and atmospheric rivers are two ways that nature is delivering the same problem: too much water, too fast, in the wrong place. Rain bombs are sudden, extremely intense downpours that dump months’ worth of rain in a few hours over a small area. Atmospheric rivers are long, narrow plumes of moisture in the sky that can deliver days of relentless rain to a region—both can trigger flash floods, landslides and huge insurance losses. This ‘river of cars’ from the tragic flood in Valencia Spain illustrates previously unknown climate impacts.[12]

A warmer planet loads the dice for these new extremes. Warmer air holds more water vapour, roughly 7% more for every degree of warming. The resulting higher humidity mainly exists as gas rather than liquid. Higher humidity means that when storms form they often have far more moisture to dump in the form of “rain bombs”, flash floods and swollen rivers, with rain that is less frequent but heavier. Extra heat also puts more energy into the atmosphere, sharpening temperature contrasts and fuelling the strong updrafts that drive large hail, damaging winds and severe convective storms.[13] On land, higher temperatures dry out soils and vegetation faster, creating longer, more flammable fire seasons where a single spark can turn into a fast-moving megafire.

These weather perils are “secondary” only in name. In many years, they now account for the majority of insured catastrophe losses. The famous primary-peril event Cyclone Tracy that destroyed the town of Darwin in Australia in 1974 caused less insured loss than the 1999 Sydney hailstorm – a classic secondary peril.[14] Severe thunderstorms, wildfires and floods are rising rapidly in both frequency and cost as the climate warms, and are now a central driver of the hardening global reinsurance market.[15]

For business planners, the important point is that not just the “big ones” hurt. It is the accumulation of many mid-sized events, happening more often, in more places, pushing loss curves and risk models beyond their historical calibration. This is exactly what a darker, hotter planet is expected to do: add energy to the system, shift baselines, and make formerly rare extremes more common.

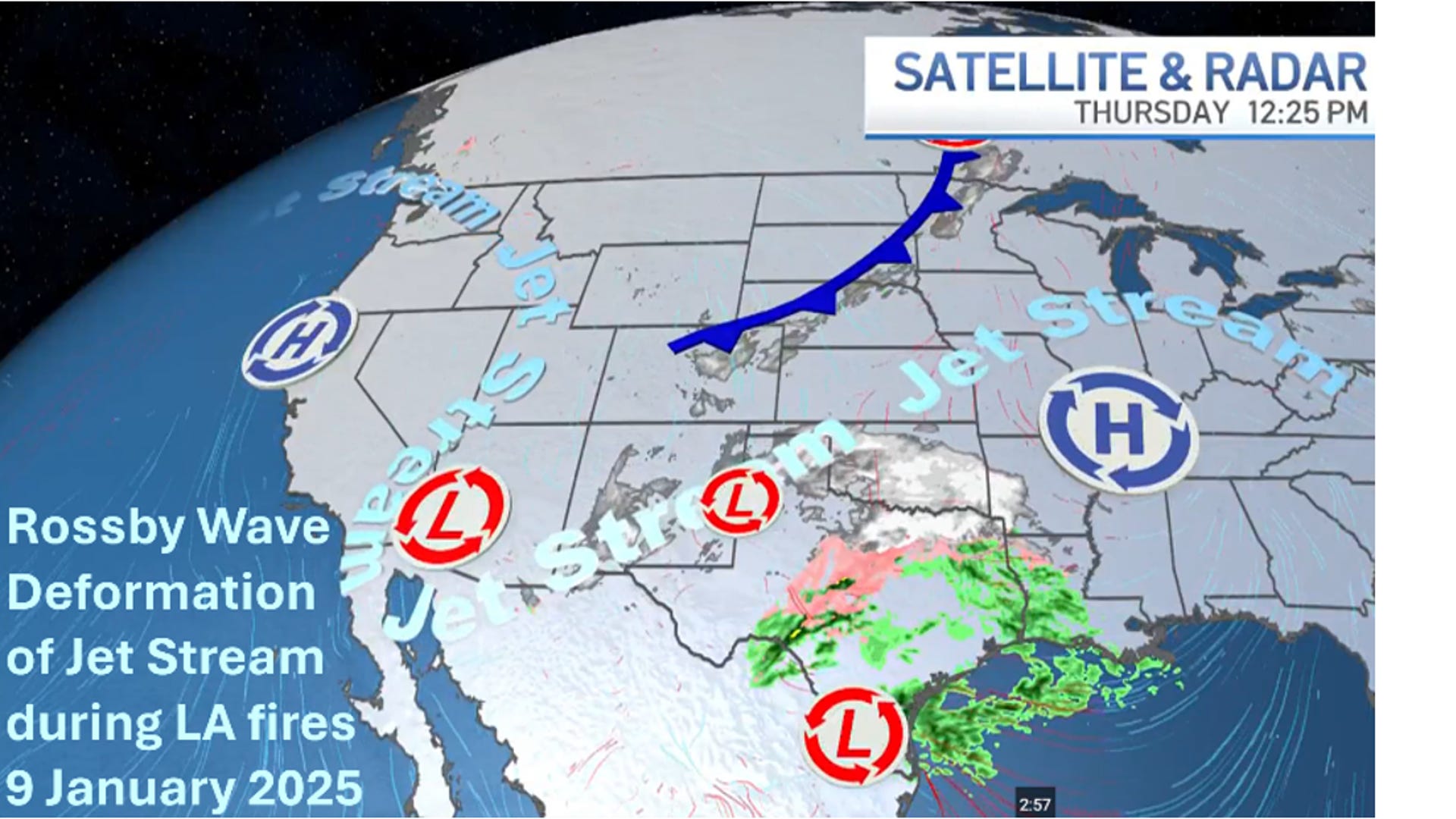

Because the whole system is more energised, weather patterns are more prone to “stall” in place, meaning the same region can endure days of unbroken downpours or weeks of extreme heat and drought. One cause of this stalling, for example with the Los Angeles 2025 fires, is the disruption of the jet stream, which used to provide a stable barrier between the tropics and the poles, but is now increasingly wayward and wavy. All of this shows up directly on insurance balance sheets as more frequent and more expensive claims.

A main cause of jet stream disruption is rapid Arctic warming. The Arctic is heating about four times faster than the global average,[16] which weakens the temperature contrast between the pole and the tropics. This contrast powers and straightens the jet stream, holding the main patterns known as Rossby Waves[17] in place. As that polar gradient softens, the jet stream becomes wavier and slower, allowing “heat domes” to park over regions and bake them for weeks, and letting tongues of polar air plunge much further south than before.[18] The result is a strange new pattern in which the same underlying cause – Arctic amplification – can give both record-breaking summer heatwaves under stalled high-pressure systems and sudden, severe winter cold snaps when the polar vortex is displaced.

Case study 1: Los Angeles 2025 Fires

The Los Angeles fires of January 2025 showed a pronounced global climate signature. The deformation of the jet stream saw the polar boundary reach down to Mexico during the fires, creating adjacent high and low pressure systems over Oregon and Arizona. These highly unusual weather systems funnelled desert winds to LA. But the jet stream signature had also created the prior conditions for the winter fires. Winter rains the year before increased vegetation. Then a ‘heat blob’ sat over the North Pacific and dried California out for nine months before the fire, in large part due to Rossby Wave jet stream deformation caused by Arctic warming

.

Case Study 2: Acapulco’s overnight catastrophe – Hurricane Otis[19]

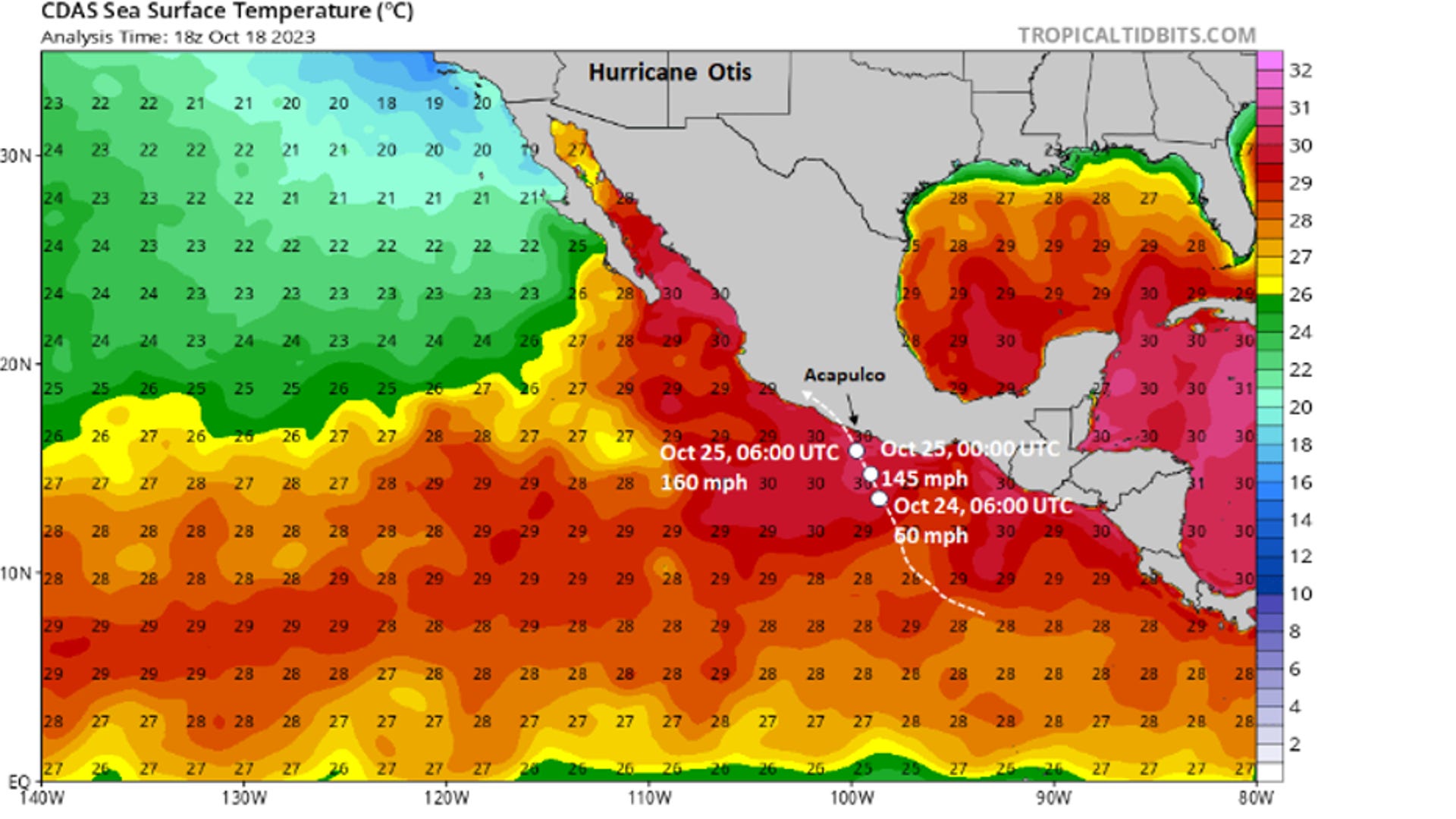

In October 2023, Hurricane Otis provided a brutal example of what “non-linear” climate risk looks like. On 24 October, Otis was a tropical storm off Mexico’s Pacific coast. In less than 24 hours, it exploded into a Category 5 hurricane, with sustained winds around 270 km/h (165 mph), before slamming directly into the resort city of Acapulco.[20] Forecasters were caught by surprise by the speed and scale of intensification, giving little warning to residents. The impact was catastrophic, with fears Acapulco may never recover.[21]

The physical backdrop was textbook climate risk. Sea-surface temperatures off the Mexican coast were exceptionally high, providing a deep reservoir of heat for the storm to tap. The heat blob of Pacific water in the path of Otis reached above 30°C. That allowed this hurricane to leap from “serious but manageable” to “once-in-a-lifetime catastrophe” in less than a day.[22]

The human and economic consequences were devastating. Dozens of people were killed; many more were injured or left homeless.[23] Much of Acapulco’s hotel stock and beachfront infrastructure was heavily damaged or destroyed. Images showed high-rise hotels with their façades ripped off, marinas smashed, roads blocked by debris. Estimates of total economic loss ran into the tens of billions of dollars; insured losses were initially put in the US $2.5–6 billion range, with substantial uncertainty given the damage to the local insurance system itself.[24] For tourism and local business, Otis was not just a bad season. It was a multi-year shock to the basic viability of the destination, from which recovery will be long and uneven.

Otis illustrates three general points:

Rapid intensification is becoming more common in warm basins, shrinking the window for evacuation and loss-reduction measures.

Traditional risk models under-price this tail risk if they rely too heavily on historical storm behaviour.

Tourism and coastal real estate are highly exposed to both physical damage and reputational risk when a “safe” resort suddenly looks like a war zone.

In a darker world, the physical conditions that powered Otis will become more frequent, pushing such surprises closer to the norm.

Case study 3: America’s $65 billion wake-up call – Hurricane Ian

Hurricane Ian made landfall in southwest Florida as a strong Category 4 hurricane in September 2022. It brought extreme storm surge, powerful winds and heavy inland flooding. Swiss Re estimated insured losses of US$50–65 billion, making Ian the second-costliest insured natural catastrophe on record after Hurricane Katrina in 2005.[25]

Ian’s legacy was not confined to the immediate disaster zone. It intensified the re-pricing of coastal risk across Florida and the US Gulf Coast, as well as accelerating the trend of private insurers withdrawing from high-risk districts. This leaves more households reliant on under-funded public schemes, pushing up premiums and deductibles, with knock-on effects for mortgage serviceability and property values.

In most markets, without insurance it is effectively impossible to get a mortgage, because banks won’t lend against a house that could be wiped out by fire, flood or storm with no guarantee they’ll recover their money. When mortgages start to disappear, it doesn’t just hurt new buyers – it destabilises the whole local economy. If banks decide an area is too risky to lend into, existing owners find they can’t refinance, potential buyers can’t get loans, and prices begin to fall. Homes that once functioned as households’ main store of wealth turn into stranded assets. Councils see their rate base erode just as they need more money for flood levees, drainage and fire protection. Local businesses struggle because both customers and lenders are wary of putting more capital into a place that may not be insurable in 10–20 years. Banks and pension funds are then left holding devalued collateral on their books, which can feed back into tighter credit conditions elsewhere. Mortgage withdrawal is therefore an early signal of a much wider balance-sheet problem: climate risk is undermining savings, investment and inheritance.

For banks, pension funds and local governments, the message is that a modern hurricane can erase tens of billions of dollars in insured value, and trigger cascading financial stress across housing markets, municipal bonds and state budgets. As the climate keeps warming, with most of this heat going into the oceans, the expected frequency of highly destructive hurricanes and similar events rises. The cost of capital will follow.

In Florida, this is no longer theoretical. After Hurricane Andrew in 1992, 11 insurers were bankrupted and many others stopped writing or renewing policies in the state. Almost a million coastal homeowners suddenly couldn’t find private insurance; the state had to create Citizens Property Insurance, an “insurer of last resort,” to stop whole suburbs becoming uninsurable and effectively unsellable.

A generation later, Hurricane Ian in 2022 repeated the pattern in southwest Florida. A 10–15-foot storm surge obliterated large parts of Fort Myers Beach and nearby communities, and one mid-sized insurer (United Property & Casualty) collapsed under roughly 25,000 claims with reported losses of over $800 million. For many homeowners in the hardest-hit streets, the numbers stopped adding up: rebuilding to new flood and wind codes cost more than the house was worth, private insurance disappeared or became unaffordable, and banks grew wary of lending into those neighbourhoods. Properties that had once been normal middle-class homes became stranded assets – technically still there on paper, but impossible to insure on commercial terms and only saleable, if at all, at deep discounts to cash buyers willing to gamble on the next storm.

When repeated hurricanes push insurance out of a market and force buyers to pay cash or unaffordable premiums, houses stop functioning as reliable collateral. In practical terms they cease to be normal assets and start to behave like stranded ones – sitting on the coast, exposed to the next landfall, with their market value and ability to secure loans eroding every season as the ocean gets relentlessly hotter, providing even more fuel for future superstorms.

Case study 4: When the river owns the town – the Lismore floods

In early 2022, the Australian town of Lismore became a symbol of what “uninsurable” looks like on the ground.

Located in the Northern Rivers region of New South Wales, Lismore sits at the junction of several rivers. Floods are part of its history. But the events of February–March 2022 broke the frame. A series of intense rain events produced record-breaking river heights, overtopping the town’s levee and inundating the central business district and surrounding suburbs, some houses up to their roofs.[26] Many residents experienced not one but two major floods in quick succession as the system re-intensified. Across eastern Australia, the 2022 floods triggered about 245,000 insurance claims and was the country’s costliest flood event on record.[27]

In Lismore and nearby towns, the impacts have been brutal. Whole neighbourhoods effectively written off as too risky to rebuild in place. Sharp increases in premiums where cover is still available, and outright withdrawal of flood insurance in the most exposed areas.[28] Widespread concerns about mortgage stress, negative equity and the long-term viability of the local economy.

Residents talk about their “one-in-a-hundred-year” flood arriving twice in a month. Statistically, that imprecise phrase captures the truth that supposedly rare events now seem to happen all the time.

From an actuarial risk assessment perspective, what has changed is not just rainfall totals, but the interaction of heavier downpours with land-use, drainage and settlement patterns. Many rain patterns are changing from steady and light to random and intense. A warmer atmosphere holds more water and can dump it more heavily. Combined with a darkening planet that absorbs more solar energy, the result is a water cycle with sharper, more damaging swings.

For lenders, developers and infrastructure owners, Lismore is a warning. Without credible plans to cool and re-stabilise the climate, the map of “bankable ground” is shrinking.

The Climate Scorpion – planetary solvency and the sting in the tail

The UK Institute and Faculty of Actuaries, together with the University of Exeter, published a report with a striking title: Climate Scorpion: the sting is in the tail.[29] This report was the second in an annual series that now includes four studies of the insurance impact of global warming. The dangerous conclusion from an actuarial perspective is that the world economy may now effectively be ‘trading insolvent’ due to the systemic failure of short term business thinking to manage climate risk.

The scorpion metaphor reflects the emerging nature of climate risk. Damage does not align smoothly to temperature, but exhibits what the actuaries call a “fat tail”. That is statistic-speak for rare high-impact outcomes. Saying ‘the sting is in the tail’ means the standard bell curve, where rare events at each end are equally likely, is now heavily skewed so catastrophes are more likely. Abrupt changes in ice sheets, circulation patterns, clouds and ecosystems are dramatically worsening damage. As noted above, leading reinsurers have calculated that the cost of climate damage is doubling every decade. Previously such ‘tail’ events on the probability distribution were discounted as rare, but now the insurers have to cope with massive payouts as fat tail risk becomes the lived reality of destroyed communities.

In traditional risk models, the most extreme “tail” events – the massive hurricanes, floods and fire seasons – were treated as rare outliers. They were safely ignored on the thin tail of the bell curve, several standard deviations from the mean. Insurance pricing could ignore them, expecting that a rare catastrophe in one region could be funded by reinsurance from other unaffected regions. But now too many regions are affected, too frequently. While not yet making insurance unprofitable, the sting in the tail of the climate scorpion analysis of recent loss data is that really big disasters are happening more often than old statistics predicted. The climate is proving to be more sensitive than models assumed. The probability curve is no longer a symmetrical bell: the right hand edge is thicker, meaning severe, system-shaking events carry much more weight. Insurers and reinsurers cannot treat these as freak occurrences any more. Climate disasters are now part of the expected pattern. That worsens risk pricing, capital requirements and business viability.

To grapple with this, the authors of the Climate Scorpion report series introduce the concept of ‘planetary solvency’. This is a way of asking whether the global economy can remain solvent under plausible climate trajectories. In other words: can the planet, as a balance sheet, absorb the shocks implied by continued warming, or does it face a form of insolvency where losses overwhelm adaptive capacity?

The Climate Scorpion report concludes that on current paths, especially beyond 2 °C of warming, the risk of “insolvency” rises sharply. For actuaries, the sting is not just the steady rise in average losses, but the possibility of sudden, compound shocks with fat tail risks that break the system’s ability to cope.

The implication for business is blunt: climate stability is not just an environmental ideal; it is a precondition for the solvency of major sectors – including insurance, banking and sovereign finance. And unfortunately, energy sector reform to switch to wind and solar is far too small and slow to mitigate these systemic business risks. Any serious conversation about risk must therefore ask not only how to reduce emissions, but how to reduce the planet’s heat imbalance quickly enough to avoid the poisonous sting of the scorpion’s tail.

What this means for the wider economy

If insurers cannot price or carry the risk, others are left holding the bag. Banks and investors face higher default risk and stranded assets as properties in high-risk zones lose value and cannot secure a mortgage. Real estate and tourism see their business models undermined by repeated disasters and the perception of danger, even in years without major events. Agriculture and food systems face greater yield volatility and more frequent local crop failures. Energy and utilities must cope with higher peak loads during heatwaves and more frequent disruption from storms, fires and floods. Defence and security communities increasingly view climate as a “threat multiplier”, stressing fragile states, fuelling migration and complicating strategic planning.[30]

In many cases, the pinch point is not abstract climate change, but a very concrete triad:

rising frequency and intensity of damaging events

rising cost and shrinking availability of insurance

falling confidence that “the past is a guide to the future”

That is why insurers and actuaries are some of the clearest voices now warning that the climate system is moving into unfamiliar territory. But these voices are swamped by the complacent assertion that energy sector reform is the main climate agenda. The bottom line is that the insurance sector now needs to champion the case for sunlight reflection to insure system viability.

From uninsurable risk to the case for cooling

The events described in this chapter have a common physical driver. Our planet is taking in much more energy than it radiates back to space. Darker oceans and shrinking bright surfaces (ice, snow, reflective clouds) are caused by and amplify that imbalance. The water cycle is running hotter, providing more water and heat as fuel for storms, floods and heatwaves.

Traditional climate policy has largely approached this as a carbon problem: adjust emissions trajectories, and long-term temperature will follow. It is like how economists sometimes talk as if what really matters is that things balance out “in the long run”: adjust interest rates or emissions trajectories, and eventually the system will drift back toward equilibrium. John Maynard Keynes famously skewered that mindset with the line, “In the long run we are all dead.” His point was that policy has to deal with the time horizons people actually live and plan in – years to decades, not centuries. Climate policy built on “get emissions right and the temperature will follow in 100–200 years” makes the same mistake. Boards, insurers and governments don’t operate on geological timescales. They need to know whether the next 10–30 years will stay within insurable, investable bounds – and that requires a direct cooling lever, not just promises about eventual carbon alignment.

For insurers, lenders and asset owners operating on 10–30-year horizons, that framing is increasingly inadequate. Even the most ambitious decarbonisation could not by itself deliver a cooler or more stable climate on those time scales. The events affecting balance sheets today are driven by current planetary heating and darkening, not by emissions that may or may not be avoided decades from now.

This is where the rest of the book will go. Planetary reflectivity (albedo) now needs to be treated as a core business risk variable, alongside emissions and CO2 concentrations. Governing sunlight reflection – in effect, rebrightening the planet – can directly reduce the fuel for extreme events. An Albedo Accord, modelled structurally on the Montreal Protocol, is a way to manage that cooling function as a public good.

For now, the takeaway for business readers is simple. The world is drifting towards a state where key regions, assets and sectors become uninsurable. If that process continues, no portfolio is safe. Cooling the planet – bringing the planetary energy budget back towards balance – is not an optional extra. It is central to preserving solvency, liquidity and long-term value.

[1] https://www.swissre.com/institute/research/sigma-research/sigma-2026-01-natcat-2025-wildfire-storm-risk/global-natcat-losses-2025.html

[3] https://www.munichre.com/en/risks/natural-disasters.html

[9] https://www.munichre.com/en/solutions/for-industry-clients/natcatservice.html

[12] https://www.theguardian.com/world/2024/oct/31/why-were-the-floods-in-spain-so-bad-a-visual-guide

[13] https://www.unsw.edu.au/newsroom/news/2025/07/warmer-with-a-chance-of-ice-hailstorms-could-hit-australian-cities-harder

[16] https://climate.mit.edu/explainers/polar-jet-stream-and-polar-vortex

[17] https://paulbeckwith.net/2021/04/17/linking-mid-latitude-extreme-weather-events-to-arctic-amplification-complexities-abound/

[18] https://egusphere.copernicus.org/preprints/2022/egusphere-2022-148/egusphere-2022-148.pdf

[19] Map Source: https://fosstodon.org/@AkaSci/111293212046621137

[21] https://nuricumbo.com.mx/why-this-may-be-the-end-of-acapulco/

I still prefer Albedo Protocol like Kyoto and Montreal. Accord sounds to *war" -ish